The congestion pricing program was instituted in January 2025 and during its first year in operation, congestion pricing raked in more than $550 million for the MTA’s $15-billion capital program.

If lawmakers believe that detention facilities are inconsistent with state priorities, then legislation should be considered that restricts the purchase or operation of such facilities within state borders.

Long-term mortgage rates can be expected to trend lower because lower inflation means less added premium to borrow money. But rates will not return to the 4%–5% range that occurred during Trump’s first term.

Editor’s Note: This article first appeared on Realtor Magazine Media. Reprinted with permission from the National Association of Realtors.

The past year was another terrific one for homeowners. Their overall net housing equity swelled to $35 trillion in 2024. Nearly a third of that growth came in the past four years. It is, therefore, not surprising that consumers who’ve bought and sold recently continue to rate very highly the real estate agent with whom they worked. Nearly nine in 10 consumers would recommend their real estate agent or broker to their friends, business colleagues, and other family members. It’s quite reassuring in the free market, with so many competing brokerage models, including do-it-yourself options, that consumers want to work, and are happy, with their specific real estate professional.

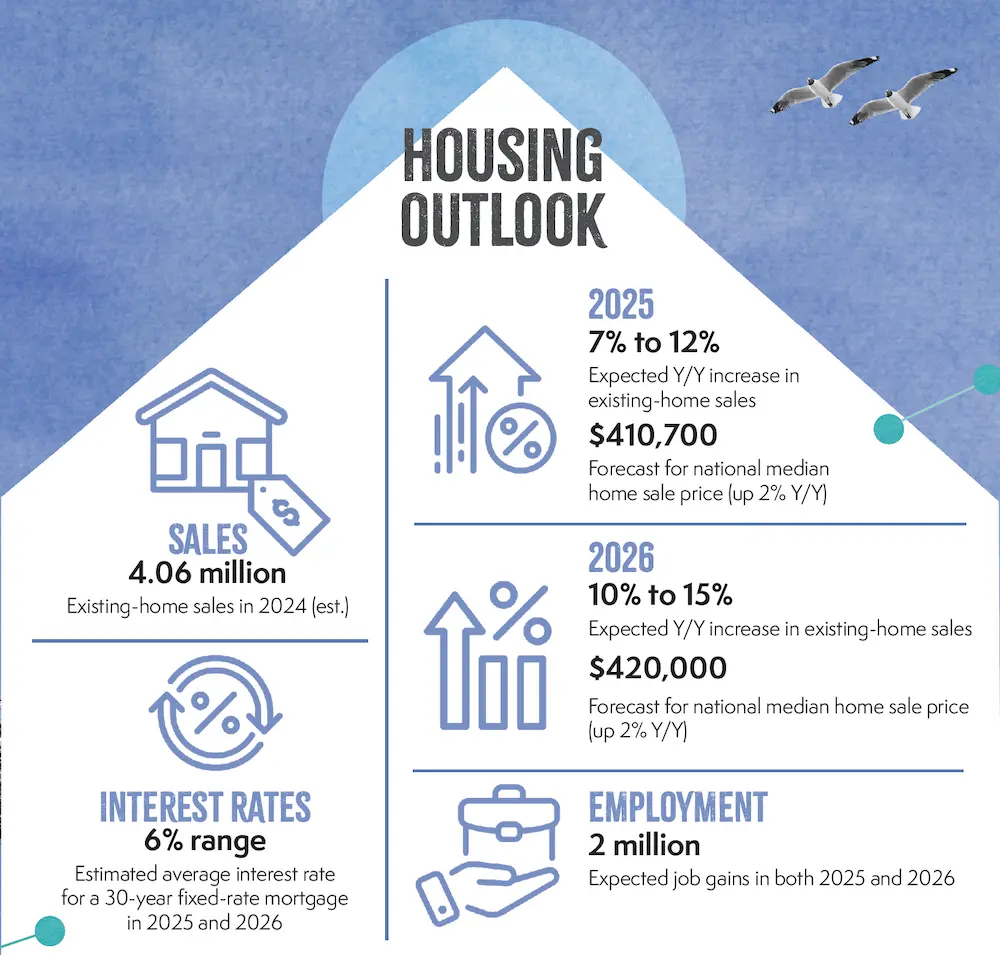

That said, it has been a difficult couple of years for real estate brokers and agents, mortgage lenders, title insurers, moving truck companies, and others whose businesses depend on real estate sales. The years 2023 and 2024 marked the slowest home sales in nearly 30 years, and housing affordability hit historic lows.

All is expected to change for the better this year. The momentum of higher home sales was already noted in the final months of 2024. A steady boost in inventory, starting in the summer months, has brought more options and excitement to those looking to buy. Incomes have been rising a shade above home price appreciation. The Federal Reserve has been cutting its short-term bank lending rate, even though mortgage rates have not followed the downward path—at least not yet. And the election and transition of power are behind us.

During President Donald Trump’s first term, a total of 21.8 million existing homes and 2.7 million newly constructed homes were sold. Under President Joe Biden, the figures were 19.3 million and 2.8 million. It would be silly to attribute sales directly to the presiding administration’s policies. The arrival of the ugly COVID-19 virus, independent monetary policy, compromises with Congress, and so many other external factors influence home sales. But one can be confident that, over the next four years, existing-home sales will easily reach 20 million—along with a solid 3.5 million new-home sales.

Why?

The high mortgage rates of 7% and 8% are over. The Fed will make further rate cut decisions in 2025 to move toward non-restrictive money policy. That’s because the overall consumer price inflation, which the Fed constantly mentions as its top goal, will be contained.

One thing that has held back the Fed is rent inflation. But in that arena, government data still lags the real world. The number of newly completed apartment units that reached the market in 2024 was 560,000, the highest since the early 1980s. Leasing activity has risen, but such a massive supply has raised vacancy rates. It’s no surprise, therefore, that various sources from the private sector are indicating essentially no rent gains in 2024. The official and somewhat fuzzy public data on rent in the consumer price index shows a 5% rise. It’s just a matter of time for the official figures to reset lower. The Federal Reserve can declare victory in having brought the inflation rate to its desired goal in 2025 and thereby permit more cutting of the short-term bank borrowing rate.

Long-term mortgage rates can be expected to trend lower because lower inflation means less added premium to borrow money. But rates will not return to the 4%–5% range that occurred during Trump’s first term. That’s because the national debt has risen from $20 trillion in 2017 to now $36 trillion. Government borrowing is not a free lunch. It’s eating up private capital, leaving less for mortgage lending than would otherwise be available. The new normal for mortgage rates will be between 6% and 7%.

A potential wild card is what Elon Musk and Vivek Ramaswamy do to slash government spending. If meaningful progress can be made to reduce spending, then mortgage rates may be able to slide into the mid-5% range. It should be worth mentioning that a majority of government spending is on promised entitlements that can not be touched, such as Social Security and Medicare.

Some in the new Trump administration will push for privatization of Fannie Mae and Freddie Mac. However, privatization is unlikely. The implied government guarantee on most mortgages (such as those originated by your local lender and later sold to Fannie or Freddie) allows for 30-year borrowing, something not available in most other countries. These guarantees also bring slightly lower interest rates and the ability to refinance at a reasonable cost.

FHA and VA lending programs have an explicit government guarantee. The intense bidding wars of a few years ago left FHA and VA borrowers at a distinct disadvantage, but as housing markets see more supply, we are likely to see more buyers who qualify opting to use those programs.

The economy and jobs are other positive factors for home sales. Gross domestic product grew by nearly 3% recently, and job gains have been ongoing. The housing demand pipeline, therefore, has been filling up. It’s just a matter of more inventory and stable mortgage rates to transform dreams of ownership into realization.

Relief for Commercial Markets

The strength of the economy going into 2025 is good news for commercial real estate. More jobs mean more retail shopping, online shopping with deliveries from warehouses, and leasing of apartment spaces. Property management and leasing business will be on the rise.

With a few more rate cuts by the Fed expected, along with lower inflation and lower loan premiums, refinancing interest rates on commercial loans will be a bit lower than last year.

Rents will rise...

In the retail sector due to very limited new construction.

In the apartment sector, though more noticeably beginning in 2026 after the market has had time to absorb newly released vacant units.

In the industrial sector because online shopping growth will outpace brick-and-mortar shopping.

Office is a different story. Although there has been job growth in what had once been called the “office-using” jobs—service professions such as accounting and management consultancy, legal and financial services—office demand has not risen. In fact, the official vacancy rate, which currently is at historic highs, does not account for many spaces that are used only two or three days a week. This inefficient and costly underutilization will work itself out over time. More subleasing spaces will hit the market. The continued rise in vacancy rates will require rent concessions to draw new tenants.

So, what about commercial real estate investment deals, which have been crushed even more so than residential home sales in the past two years? There’s no government guarantee on commercial loans (aside from some multifamily loans), and therefore, borrowing is of a short duration—generally three, five or seven years.

Many loans made during the early period of COVID-19, when rates were super low, are coming due. Around $2 trillion in loans need to be refinanced at higher interest rates over the next two to three years. Moreover, the lack of investment deals has brought commercial property prices well below the pre-pandemic levels of 2019. Lower collateral value means needing to bring some cash to the table for refinancing. The extension of loans is buying time, even at some cost to lenders. But granting an extension is still less costly for a lender than foreclosing and selling the property at a deep discount.

If lawmakers believe that detention facilities are inconsistent with state priorities, then legislation should be considered that restricts the purchase or operation of such facilities within state borders.

The region’s housing crisis has become a commercial real estate constraint. Limited housing availability affects workforce retention, which in turn impacts employers’ willingness to expand or relocate.

Receive original business news about real estate and the REALTORS® who serve the lower Hudson Valley, delivered straight to your inbox. No credit card required.