The congestion pricing program was instituted in January 2025 and during its first year in operation, congestion pricing raked in more than $550 million for the MTA’s $15-billion capital program.

If lawmakers believe that detention facilities are inconsistent with state priorities, then legislation should be considered that restricts the purchase or operation of such facilities within state borders.

WASHINGTON—Approximately 90% of metro markets (196 out of 226, or 87%) registered home price gains in the third quarter of 2024, as the 30-year fixed mortgage rate ranged from 6.08% to 6.95%, according to the National Association of Realtors’ latest quarterly report.

Seven percent of the 226 tracked metro areas recorded double-digit price gains over the same period, down from 13% in the second quarter.

“Home prices remain on solid ground as reflected by the vast number of markets experiencing gains,” said NAR Chief Economist Lawrence Yun. “A typical homeowner accumulated $147,000 in housing wealth in the last five years. Even with the rapid price appreciation over the last few years, the likelihood of a market crash is minimal. Distressed property sales and the number of people defaulting on mortgage payments are both at historic lows.”

Compared to one year ago, the national median single-family existing-home price ascended 3.1% to $418,700. In the prior quarter, the year-over-year national median price increased 4.9%.

Among the major U.S. regions, the South registered the largest share of single-family existing-home sales (45.1%) in the third quarter, with year-over-year price appreciation of 0.8%. Prices also increased 7.8% in the Northeast, 4.3% in the Midwest and 1.8% in the West.

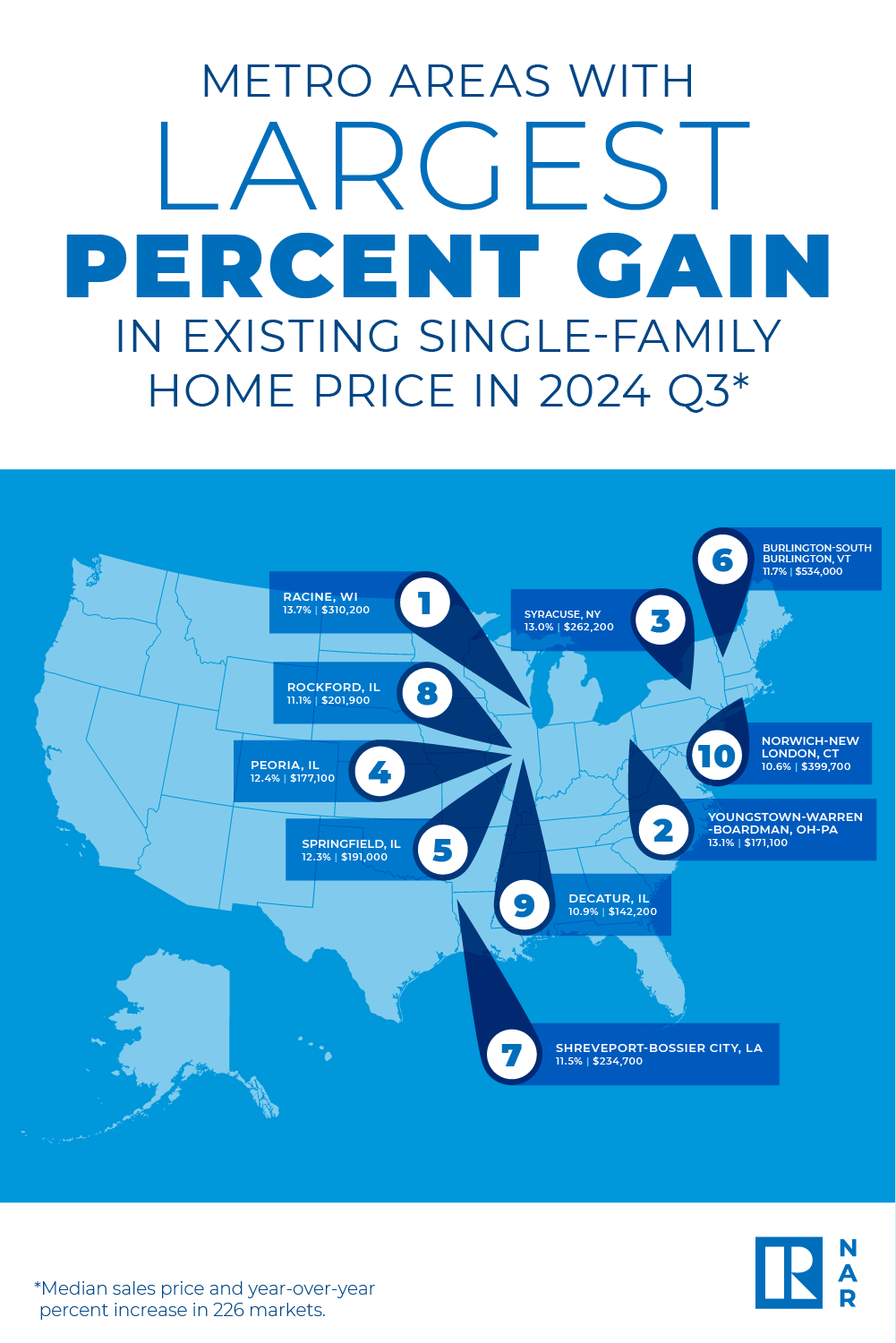

The top 10 metro areas with the largest year-over-year median price increases, which can be influenced by the types of homes sold during the quarter, all experienced gains of at least 10.6%. Four of the markets were in Illinois. Overall, those markets were Racine, WI (13.7%); Youngstown-Warren-Boardman, OH-PA. (13.1%); Syracuse, NY (13.0%); Peoria, IL (12.4%); Springfield, IL (12.3%); Burlington-South Burlington, VT (11.7%); Shreveport-Bossier City, LA (11.5%); Rockford, IL (11.1%); Decatur, IL (10.9%); and Norwich-New London, CT (10.6%).

Eight of the top 10 most expensive markets in the U.S. were in California. Overall, those markets were San Jose-Sunnyvale-Santa Clara, CA ($1,900,000; 2.7%); Anaheim-Santa Ana-Irvine, CA ($1,398,500; 7.2%); San Francisco-Oakland-Hayward, CA ($1,309,000; 0.7%); Urban Honolulu, HI ($1,138,000; 7.2%); San Diego-Carlsbad, CA ($1,010,000; 3.2%); Salinas, CA ($959,800; 1.5%); San Luis Obispo-Paso Robles, CA ($949,800; 6.7%); Los Angeles-Long Beach-Glendale, CA ($947,500; 5.6%); Oxnard-Thousand Oaks-Ventura, CA ($947,400; 2.8%); and Boulder, CO ($832,200; -3.0%).

Nearly 13% of markets (29 of 226) experienced home price declines in the third quarter, up from almost 10% in the second quarter.

Housing affordability slightly improved in the third quarter as mortgage rates trended lower. The monthly mortgage payment on a typical existing single-family home with a 20% down payment was $2,137, down 5.5% from the second quarter ($2,262) and 2.4%—or $52—from one year ago. Families typically spent 25.2% of their income on mortgage payments, down from 26.9% in the prior quarter and 27.1% one year ago.

“Housing affordability has been a challenge, but the worst appears to be over,” Yun said. “Rising wages are outpacing home price increases. Despite some short-term swings, mortgage rates are set to stabilize below last year’s levels. More inventory is reaching the market and providing additional options for consumers.”

First-time buyers found marginally better affordability conditions compared to the previous quarter. For a typical starter home valued at $355,900 with a 10% down payment loan, the monthly mortgage payment declined to $2,097, down 5.5% from the prior quarter ($2,218). That was a decrease of $49, or 2.3%, from one year ago ($2,146). First-time buyers typically spent 38% of their family income on mortgage payments, down from 40.6% in the previous quarter.

A family needed a qualifying income of at least $100,000 to afford a 10% down payment mortgage in 42.5% of markets, down from 48% in the prior quarter. Yet, a family needed a qualifying income of less than $50,000 to afford a home in 2.2% of markets, down from 2.7% in the previous quarter.

The congestion pricing program was instituted in January 2025 and during its first year in operation, congestion pricing raked in more than $550 million for the MTA’s $15-billion capital program.

The 1.15 million-square-foot retail center, which originally housed 30 stores when it opened in 1954, is now home to more than 100 retail, dining, educational and entertainment venues.

Receive original business news about real estate and the REALTORS® who serve the lower Hudson Valley, delivered straight to your inbox. No credit card required.