The cost of acquiring the vacant 12.43-acre site is $3.9 million. According to its application with the IDA, building and construction is estimated to cost $17,864,850 and equipment costs have been put at $13,136,536.

Bally’s Bronx, as proposed to the New York State Gaming Commission late last month, was to stand approximately 250 feet tall and include a 500,000-square-foot Gaming Facility structure and span more than 3 million square feet.

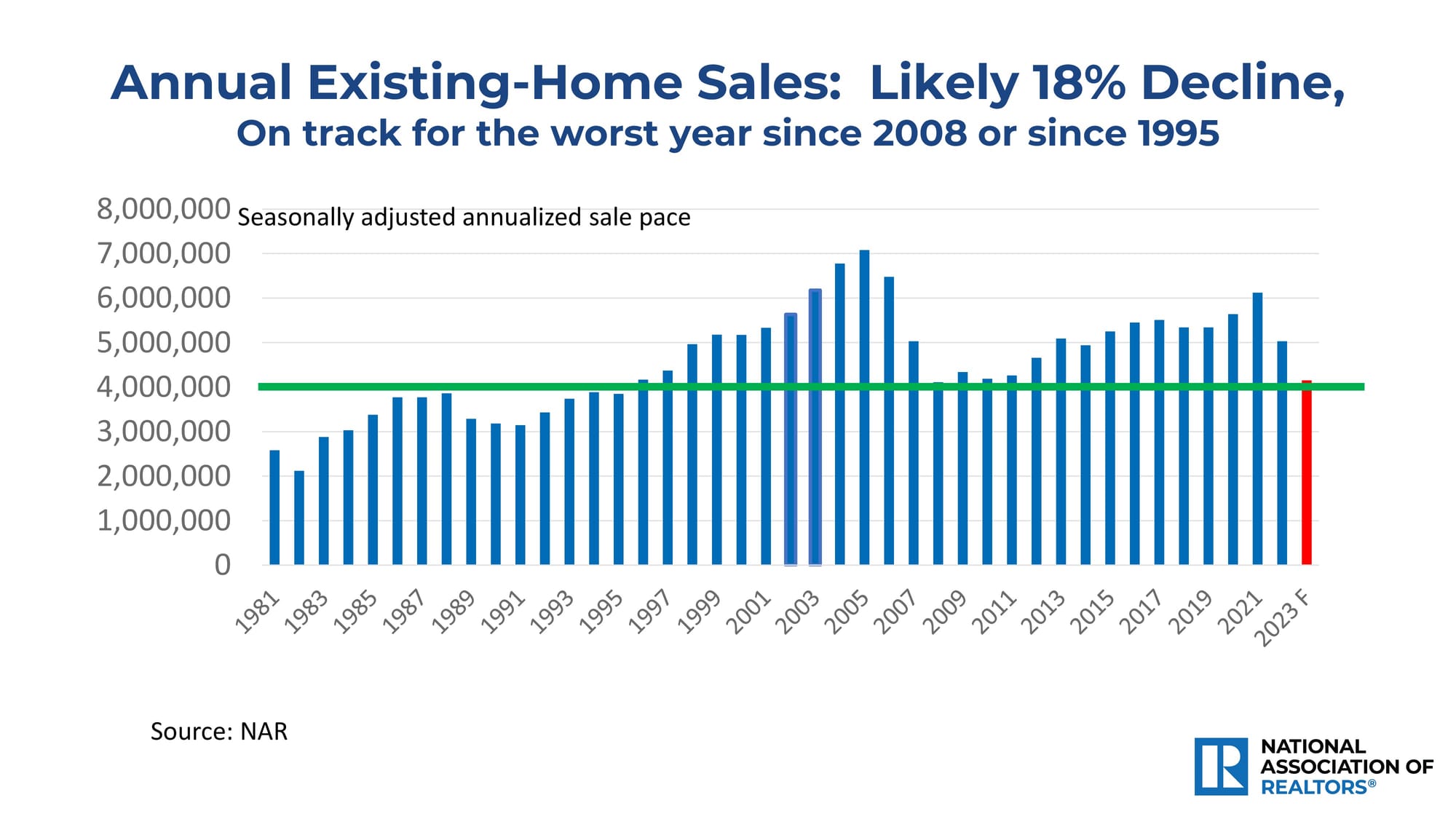

WASHINGTON—A day before the Federal Reserve decided to hold rates steady and indicated it foresees three interest rate cuts in the coming year, the National Association of Realtors held its annual Real Estate Forecast Summit, which reviewed a rather tumultuous 2003 and an improving market in 2024.

The virtual panel included Dr. Lawrence Yun, Chief Economist and Senior Vice President of Research, National Association of Realtors; Dr. Jessica Lautz, Deputy Chief Economist and Vice President of Research, National Association of Realtors; Danielle Hale, Chief Economist, Realtor.com; Danushka Nanayakkara, Assistant Vice President for Forecasting and Analysis, National Association of Home Builders; Ken Simonson, Chief Economist, Associated General Contractors of America and Dr. Caitlin Sugrue Walter, Vice President of Research, National Multifamily Housing Council.

NAR’s Yun noted that high-interest rates and low inventory once again battered the existing home sales market, posting an 18% decline in sales in 2023, which followed a lackluster 2022 when the market also experienced an 18% drop in sales from the prior year. Depending on how the market performs in the last two months, the existing home sales market is on pace for its worst year since 2008 or 1995, according to NAR data. New home sales, however, are on track for the third or fourth best years since 2008 and were up 4.5% year-to-date in October 2023. He expects existing and new home sales to increase 13% respectively in 2024.

While accurately predicting that the Federal Reserve would hold interest rates steady the next day, Yun related that if the Fed were to use the private sector apartment data, the nation’s inflation rate would be at the Fed’s 2% target level and it would therefore be time for the Fed to begin to cut rates. Yun noted that once the official data catches up with the private sector apartment numbers, the Fed will seriously consider cutting interest rates.

One of the factors that could influence when the Federal Reserve will begin to cut rates is the softening jobs market in a Presidential election year.

Yun forecasts that U.S. GDP will grow by 1.5%, avoiding a recession, with net new job additions slowing to 1.7 million in 2024, compared to 2.7 million in 2023 and 4.8 million in 2022.

After eclipsing 8% in late 2023, he expects the 30-year fixed mortgage rate to average 6.3% in 2024 and that the Fed will cut rates four times—calming inflationary conditions—in response to slower economic activity. He predicts the first rate cut by the Federal Reserve will come in the late spring.

Yun expects rent prices to calm down further in 2024, which will hold down the consumer price index. He predicts foreclosure rates will stay at historically low levels in 2024, comprising less than 1% of all mortgages.

“The demand for housing will recover from falling mortgage rates and rising income,” Yun said. “In addition, housing inventory is expected to rise by around 30% as more sellers begin to list after delaying selling over the past two years.”

Yun also foresees 1.48 million housing starts in 2024, including 1.04 million single-family and 440,000 multifamily.

Realtor.com’s Hale was in agreement that the market will improve in 2024, but offered a number of differing views on mortgage rates. In Realtor.com’s recent housing forecast for 2024, Hale said that mortgage rates will average 6.8% for the year and reach 6.5% by the end of the year. Home prices will ease slightly and drop by 1.7% after generally increasing since 2012. Rents are expected to drop by 0.2%. Home sales are expected to hold steady, rising 0.1% year over year to 4.07 million.

“Our 2024 housing forecast reveals the green shoots we’ve been waiting to see in the housing market and should give buyers some optimism after a grueling few years. Although mortgage rates are expected to ease throughout the course of the year, the continuation of high costs will mean that existing homeowners will continue to have a high threshold for deciding to move, but we will start to see some interest,” said Hale. “Moves of necessity—for job changes, family situation changes, and downsizing to a more affordable market—are likely to drive home sales in 2024. Home buyers will continue to seek out markets where they feel like they get the most out of their dollar as they look for homes that better meet their needs.”

Among Realtor.com’s key housing trends and wildcards include its belief that affordability will turn around in 2024. “In 2024, the typical monthly purchase cost for the median-priced home listing is expected to be slightly less than $2,200/month, or about 35% of the typical household income. That’s an improvement from 2023 when purchase costs ate up nearly 37% of income and the typical for-sale home cost $2,240. This tick up in affordability will give a foothold to some buyers trying to break into the market,” the report stated.

In addition, the pace of rate cuts and the expected decline in the 30-year mortgage rate could determine inventory levels going forward. “Despite the fact that builders have been catching up, the lack of excess capacity in housing has been obvious over the last few years. With home sales activity forecasted to continue at a relatively low pace, the number of unsold homes on the market is also expected to remain low. But if rates drop faster than expected (which is possible given the roughly half-point decline seen in November 2023), this could lessen rate lock sooner and bring more homes to the market than forecasted,” the Realtor.com report stated.

Leasing activity surged this quarter to over 360,000 square feet, a 45% increase from the first quarter of this year, with renewals representing 57% of executed transactions.

The One Big Beautiful Bill Act includes multiple NAR-championed provisions designed to support homeownership, drive investment in housing supply, and strengthen the real estate economy.

Receive original business news about real estate and the REALTORS® who serve the lower Hudson Valley, delivered straight to your inbox. No credit card required.